Whether for your payments, inventory, or cash flow, our financing solutions help you move forward with peace of mind.

Embedded credit 2025: 9 stats signaling the next fintech focus

Europe is in the middle of a financial technology reformation. Riding a wave of new regulations, open banking advancements, and entrepreneurial initiative, the consumer and business banking experience today is unrecognizable to those looking back just 10 years.

Companies like Wise, Revolut, Monzo, Adyen and Klarna took seemingly intractable pain points and fundamentally reshaped the way money moves.

I’m fully convinced that lending—to small businesses in particular—is about to take a leap. With new technology and more open banking data, everything changes.

This has the potential to drastically change the way we do business.

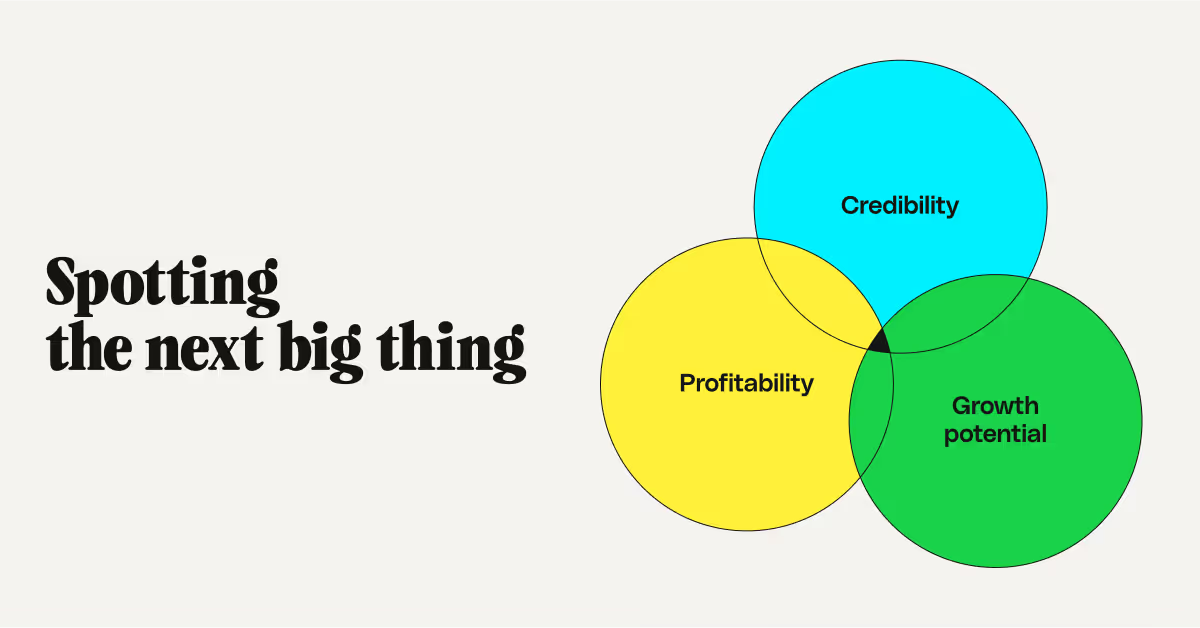

How to recognise a major tech shift

What does it take to create industry-shifting, status quo-altering innovation? For a tech innovation to create lasting change, we can look to three key factors:

- Credibility: Are the right people talking about this? In particular, are incumbent players (who benefit most from the status quo) making moves to either adopt or prevent this innovation from taking hold? That suggests there’s more than just smoke here.

- Growth potential: First, is there a significant enough market? For the “next big thing,” we’d expect it to potentially apply to the entire business landscape. And second, are we too late? If the market has already been broadly tapped, we can no longer talk about growth potential. Getting in now may be too costly and bring too little return.

76% of executives see embedded lending as a “massive” growth opportunity. And half of SMBs would willingly pay non-financial providers for the same services they currently get from banks. So the potential for major growth across industries is huge. - Profitability: Investors and incumbent players need to know that their resources spent on innovation will bring real rewards. And as AI and automation keep delivering efficiency gains, we expect new tech trends to have serious profit margins.

So that’s a basic framework to analyze any tech trend. And we can paraphrase those three factors into Is it real? Is it worth it? Why now?

B2B vs B2C embedded credit

Before we go any further, it’s worth defining the kinds of lending we’re talking about. Consumers have had mainstream embedded credit services for years now.

Think of Buy Now, Pay Later (BNPL) schemes built into Shopify, Amazon, or Vinted. These third party providers (Klarna, Affirm, PayPal Pay) deliver payments to sellers upfront, and give buyers a few weeks or months to complete their transactions.

But we haven’t seen the same widespread embedded credit for businesses. Companies have the kind of predictable, formal purchasing processes that are ideal for automation. And the number of B2B invoices processed each day is staggering—an estimated 25 billion B2B invoices are issued each year in the US alone.

So let’s dig into why embedded credit for business borrowers is about to take flight.

1. 79% of banks predict banking will be “deeply embedded” in commercial activities

Traditional banks have dominated the lending industry for centuries, and still do. But incumbents are recognising the changing role of traditional services in consumers’ and companies’ lives. Banking and credit lending aren’t going anywhere, but how people and businesses access these products is shifting.

According to PYMNTS Intelligence research, 79% of banks are looking towards a “deeply embedded” future. Much of this comes from evolving consumer expectations—neobanks like Revolut, Monzo, and N26 have reset the bar for customer service and mobile-first experiences.

Embedded services mean banking transactions will take place outside of banking branches and platforms. Business customers will be able to send, borrow, invest, and analyze capital without opening their banking app or talking to an agent.

PYMNTS found that 70% of banks do indeed see embedded finance as a “cornerstone” of their digital banking strategy, but 75% of bank executives said a lack of cohesive internal strategy was standing in the way.

Real-world embedded finance examples

- Affirm: BNPL provider Affirm has partnered with major retailers like Walmart and Peloton to offer real-time financing options directly at the point of purchase.

- Klarna: Swedish giant Klarna provides BNPL to retailers including Etsy,

Sephora, Ray Ban, Wish, Nike, Microsoft, and many more. - Square: Square has expanded its embedded lending service offerings by providing small business loans directly within its point-of-sale system.

- Inbank: The Estonian fintech gives solar panel installers a partner portal through which to offer financing to customers.

- Allegro & Vinted: These European marketplaces have built their own embedded credit services to let customers check out now, and pay in installments (another form of BNPL).

2. ~50% of financial assets are now held by non-bank intermediaries

The credit landscape has changed fundamentally in a relatively short amount of time. As Simon Taylor explains:

“For centuries, banks originated loans. You got a loan from a bank, and the bank took deposits to manage the risk of loan default. But in the wake of the banking crisis, higher interest rates, and the rise of non-bank lending from Fintech companies, the role of banks as lenders is diminishing.”

According to the Financial Stability Board, global banks (including central banks) only hold about 38% of financial assets. Meanwhile, non-bank financial intermediaries (NFBIs) hold 49%:

Image: CEPR.org. Data: Financial Stability Board (FSB), 2022

The private credit market has grown over 100% in the past five years.

This isn’t all lending. Much of this plays out in capital markets, and the asset share belonging to investment funds and private equity has also grown significantly.

But those investment funds are often lenders too, and they’re being joined by a range of new shadow banks and fintech providers. According to Taylor, this fills a market gap created by restrictions and regulations on larger banks (particularly the need to hold adequate capital in reserve), and a lack of specialization required to serve modern companies and consumers well.

3. The embedded finance market is expected to grow by 33% per year

Let’s turn now to growth potential, our second factor. According to Grand View Research, the global embedded finance market was estimated at US$83.32 billion in 2023, and is projected to grow at a compound annual rate of 32.8% from 2024 to 2030:

Source: Grand View Research

A separate report from BCG and Adyen estimated the total addressable market in 2024 at $185 billion. According to them, 80% of the addressable market remains untapped.

Source: Adyen

That’s the kind of trajectory that gets investors and entrepreneurs racing to be first. And the reasons for excitement are well known:

- Business banking and financial management are still slow, and full automation remains uncommon.

- Consumer banking has proven how efficient and pleasurable these processes can be.

- Automation and AI have made key finance steps like KYC, risk analysis, credit checks and underwriting almost instant.

- Regulatory constraints make innovation difficult for larger banks.

- But open banking and data sharing have let new players (including fintechs) into the market.

In short, we have the technology to overhaul a wide range of business financial processes. The key questions remaining are around distribution: where do we want to embed these services, and who will lead the market from early movers into the mainstream?

The ability to build banking-adjacent services into any service or platform has completely changed the finance landscape. This is what Fintech Brainfood’s Simon Taylor describes as “the biggest growth opportunity in finance.”

4. Embedded credit may account for 25% of European SMB loans by 2030

As the embedded finance market grows, so too does lending. BNPL services are already widespread, and other forms of embedded credit will follow.

In the US, the market is expected to grow from US$7.65 billion in 2024 to US$45.74 billion by 2034, a compound annual growth rate of nearly 20%. This is driven by rapid digitalization, an increasing customer demand for fast access to credit, and technological innovation.

The growth opportunities for small business lending in particular are huge. Analysis from McKinsey found that “in Europe, the embedded-finance channel accounted for 5 to 6 percent of lending revenues from retail and small and medium-size enterprises in 2023 and could reach 20 to 25 percent by 2030.”

Source: McKinsey

We know that SMBs have long been underserved by traditional banks, factoring services, and other lenders. Embedded credit provides an opportunity to fintechs and other platforms to step into this space and offer short-term financing to help our vital small businesses grow.

In turn, those banks and traditional lenders will catch up with their own embedded services. Due in part to a push from these new players, but mostly because of the low costs and the new levels of efficiency possible.

5. Embedded lending is only ⅕ as prevalent as payments

When projecting growth, it helps to look at success stories. And to find a success story of embedded finance growth, we need only look at payments.

Digital-first, online payments are now the norm for eCommerce and software businesses, and increasingly used for old fashioned utilities and rent payments. In much of Europe, you can pay your tax bills and speeding tickets directly through government websites.

Embedded lending isn’t there yet. But payments provide an excellent roadmap for what’s coming.

Despite all the clear benefits and ample opportunities that embedded credit provides, a relatively low number of tech platforms currently provide lending services. Compared with the rapid rise of payments as a service, lending is in its infancy:

Source: Matt Brown’s Notes

Matrix Partners’ Matt Brown’s analysis above is of hundreds of vertical-specific software. While some offer more than just payments, the most common combinations are payments + expenses or payments + accounting.

Lending is an interesting product offering for payments providers: if your revenue comes from customers spending through your platform, what happens when they run out of capital?

And because we know that small businesses struggle to access funding, it’s smart business to be there for them in these moments. Even better if you have customers’ accounting data and can see their cash conversion cycle, seasonal fluctuations, and other useful information.

Most importantly, payments’ adoption has proven the viability of embedded finance for software platforms. The graph above shows that there’s a range of possible followers.

We would argue that credit is best placed to be next. Companies already have good access to expenses, accounting, payroll, and other business services. But small businesses are crying out for better access to capital.

6. 83% of consumer lenders offer embedded credit vs only 45% of SMB lenders

We looked above at the differences between B2C and B2B embedded credit. The B2C side of the coin is already showing the growth opportunities for B2B lenders.

According to research from Visa and PYMNTS, over 80% of consumer lenders have at least one embedded lending product in the market. This is likely a profitability play - private individuals make even smaller and less predictable purchases than SMBs. So consumer lenders moved quickly to make their services as low-touch and automated (and therefore profitable) as possible.

But today, only 45% of SMB lenders have an embedded credit product. These lenders must rely on small business customers coming through their classic loan request processes. They’re missing the chance to reach SMBs in other forums and offer more dynamic, contextual credit.

Again, this shows the growth potential for SMB lenders. Just as we saw with the adoption of payments, consumer lenders have shown a willingness and ability to launch new embedded products.

We’re currently witnessing “a huge and material unmet need that presents an opportunity for lenders to engage and retain SMB customers,” per Visa executive Arvind Ronta. Smart SMBs use short-term financing to fund growth and overcome temporary working capital challenges.

The technology is there, and rapid advancements in open banking mean that the necessary data is now publicly available across Europe. Innovative companies have a golden moment to move, before everyone else catches on.

7. Automated underwriting decisioning has “nearly zero” marginal cost

Now we turn to the third factor in our framework: profitability. One reason for SMBs being left behind by traditional lenders is the cost involved in assessing and servicing credit. When this work is done manually, each small business customer takes a piece of the lender’s limited resources.

But, as McKinsey explains, “underwriting decisioning for lending can now be automated at nearly zero marginal cost through instant connections to public data sources such as tax records and private sources such as account transactions and balances.”

AI-powered, automated underwriting can analyze stacks of required documents, check online databases and registries, review revenue histories, and benchmark new clients against lookalikes—instantly. What previously took paid agents hours per request can now be done immediately, at scale.

Whether you offer 10 or 10,000 loans makes no real difference. The tools can complete their analyses and compliance checks, originate loans, and simultaneously onboard as many customers as you could possibly need.

Of course, there will always be some cost. That may be the initial investment in building an automated underwriting system, or ongoing payments or revenue sharing with partners.

But this represents a fraction of the costs involved in manual credit checks and lending decisioning. And crucially, the marginal cost for each individual loan is negligible.

8. Lenders with high profit margins are 23% more likely to offer embedded lending

In a survey conducted by Visa and PYMNTS, 51% of lending providers described themselves as not interested in providing embedded services. This is despite the fact that 37% of SMBs would be “very or extremely interested in switching to a service provider that offers embedded lending.”

In other words, it’s a real revenue source for lenders.

And this is already proving itself in their relative profit margins. From the same survey, “lenders with increased net profit margins are 23% more likely to have embedded credit in their portfolios than those with stable or lower net profit margins.”

This may be both correlation and causation. We’ve already seen how cost effective and efficient the processes fueling embedded credit (like automated underwriting) are. And those lenders not embedding their services elsewhere are missing out on market share.

But a lack of embedding is also correlated with further inefficiencies and operational challenges. The survey’s authors write that “technology integration and infrastructure challenges represent their biggest area of concern, cited by 34% of this group as the most significant obstacle they face in beginning to offer embedded lending products. Operational and scalability issues follow, at 23%, with risk management and credit assessments close behind, at 22%.”

Whether you believe in causation or correlation, one thing is clear: the most profitable lenders worldwide are embracing embedded credit.

9. Generating new business through embedded lending may be 15-20x cheaper for lenders

A final quote from McKinsey: “In one major European market, we found that the acquisition cost of a qualified SMB lending lead is 15 to 20 times higher than an EF (embedded finance) lead.”

The authors didn’t go into further detail, but there are several likely causes:

- Automated prospect qualification, credit analysis, and loan initiation. Remember, automated underwriting has zero marginal cost. It doesn’t require human resources, and can be done at scale (almost) instantly.

- Lenders can offer highly-customized products. Thanks in large part to AI, each new loan can be designed specifically to suit the specific customer. Still automated, and still instant. Which naturally creates much better leads and higher acceptance rates.

- Prospects can easily self-disqualify. The above automation (and an AI-powered intake process) means that bad-fit customers can quickly figure out that they’re a bad fit. This works because the origination process is so tailored to each specific user. Which would normally take significant human effort to achieve, which means additional costs.

- Embedded services meet prospects where they are. Instead of prospecting for leads, lending opportunities are available in the tools and services people already use and trust. That means more hand-raisers and less energy spent on hooking users in.

And with more partnerships and services embedded more widely, the lead generation flows in all directions. Fintechs will generate new customers by partnering with banks and non-finance software.

Non-financial platforms will attract new users who need lending built into their other business tools. And banks will reach business customers they were previously unable to unwilling to serve—most notably SMBs.

More dynamic services for lenders & small businesses

These nine key facts show what an exciting time this is for embedded finance, and credit in particular. That excitement is shared between the financial institutions who can now issue and service loans at scale for a fraction of the previous cost, and SME owners who will soon have more democratic access to the funding they so desperately need.

We’re at an inflection point, but there’s work to do yet. First and foremost, we need to see lending embedded in the core services small businesses rely on. These could be accounting and cash management tools, supplier catalogs, and factoring services.

And we hope to see more banks taking this golden opportunity to innovate. In partnership with the startups building real-time underwriting and AI-native servicing tools, banks and lenders can create new suites of products and better serve SMBs.

We have the technology, we have the demand. Let’s seize this astonishing opportunity.

See how Defacto Core lets you add automated, embedding lending to your platform.

Explore other articles

In the agent age, you won't apply for financial products. Your agent will subscribe to them.

How Defacto Built Its B2B Credit Card with Stripe Issuing

.png)